2 4 Long-duration contracts classification and measurement

For term policies without cash surrender values, the purchaser’s entire cost is recognized as a loss. Recognizing this loss in either cash surrender value of life insurance balance sheet classification circumstance is unduly conservative and unjustified. To make matters worse, a large gain is recognized when the insured dies.

- It’s essential for companies to consult with tax professionals who are well-versed in the nuances of life insurance taxation to navigate these complexities effectively.

- Your insurance company will deduct the cost of your insurance from your cash value balance.

- When you surrender a policy, you receive whatever you paid in premiums back tax-free.

- In addition, you may also be interested in knowing the cash surrender value of your policy.

- The cash value in a permanent life insurance policy grows on a tax-deferred basis.

What to do if you want to increase the cash surrendervalue of your life insurance policy

The long-term asset construction in progress accumulates a company’s costs of constructing new buildings, additions, equipment, etc. Each project’s costs are accumulated separately and will be transferred to the appropriate property, plant, or equipment account when the asset is placed into service. At that point, the depreciation of the constructed asset will begin. Long-term assets are also described as noncurrent assets since they are not expected to turn to cash within one year of the balance sheet date.

1 Investments in life insurance contracts

For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. JAMES H. THOMPSON, CPA, PhD, is professor of accounting in the Meinders School of Business at Oklahoma City University in Oklahoma.

3 Defined benefit plans

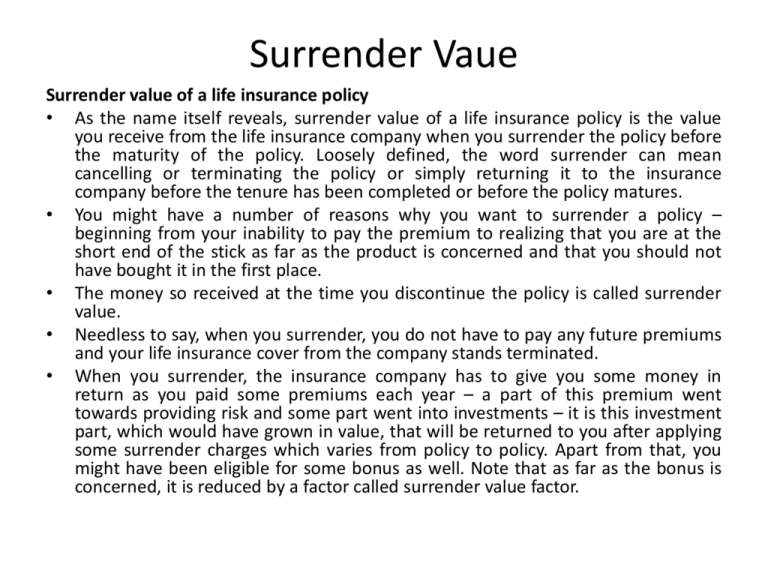

It grows slowly at first, but the value can accelerate over time thanks to the power of compound interest and earnings. In the early years of a policy, life insurance companies can deduct fees upon cash surrender. What you receive for your cash surrender value could be less than your current cash value balance after subtracting these fees.

Use the Cash Value to Cover Your Premiums

The information is presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor and might not be suitable for all investors. Investors should consider engaging a financial professional to determine a suitable retirement savings, tax, and investment strategy. Investments in common stock, preferred stock, corporate bonds, or government bonds that can be readily sold on a stock or bond exchange. These investments are reported as a current asset if the investor’s intention is to sell the securities within one year.

Sufficient cash value must remain inside the policy to support the death benefit. If you surrender your policy, you end your life insurance contract. You stop having to pay premiums and will receive all your cash surrender value. Your heirs will no longer receive a death benefit when you pass away. For example, suppose you take out a variable universal life insurance policy for $100,000. You make five years of payments and build up a cash value of $10,000.

The cash surrender value equals the policy’s cash value minus surrender fees. Any loans you’ve taken against the policy or unreimbursed withdrawals will also decrease the cash surrender value. The importance of accurately accounting for CSV cannot be overstated, as it directly influences a company’s balance sheet and overall financial health. Investopedia does not provide tax, investment, or financial services and advice.

On the other hand, the cash surrender value represents the amount available to the policyholder if the policy is terminated before the insured event occurs. Unlike the face value, the CSV is not fixed and can fluctuate based on various factors, including the premiums paid, the policy’s age, and the insurer’s investment performance. The CSV can be accessed by the corporation during the policyholder’s lifetime, offering a source of liquidity that can be used for various corporate needs, such as funding operations or investing in new opportunities. Regular reviews and adjustments are necessary to ensure the CSV is accurately represented.

Land refers to the land used in the business, such as the land on which the production facilities, warehouses, and office buildings were (or will be) constructed. The cost of the land is recorded and reported separately from the cost of buildings since the cost of the land is not depreciated. You can set the default content filter to expand search across territories. Therefore, the recorded amount of goodwill is not amortized to expense. Instead, each year the recorded cost of the goodwill must be tested to see if the cost must be reduced by what is known as an impairment loss.

This value accumulates over time as premiums are paid, and it is recorded as an asset on the balance sheet. The process of accounting for CSV begins with recognizing it as a non-current asset, given that it is not expected to be liquidated within the operating cycle of the business. Cash surrender value is money a life insurance policyholder receives for canceling their policy before it matures or they pass away. This cash value is the savings component of most permanent life insurance policies, such as whole life and universal life.

Keep in mind that taking out a policy loan, withdrawal or using the cash value to pay premiums may impact your policy’s future performance. It’s important to request a life insurance illustration every two years to monitor your policy’s projected performance. If you need cash from your life insurance policy, terminating the contract isn’t the only option.